"Many people spend money they haven't earned, buy things they don't want, to impress people that they don't like." Will Rogers

WEALTH

Across the world, people strive for a better life and long for stability, certainty, and security. Yet many remain burdened by debt, limited financial knowledge, and a lack of the skills needed to build wealth. Henry Thoreau the American poet, and philosopher once said: “The mass of people leads lives of quiet desperation.” Money allows us to meet our basic needs, cover expenses, and enjoy a greater sense of freedom and comfort. It is, undeniably, a necessity. While it’s often said that money cannot buy happiness, a more accurate perspective is that the absence of money can lead to misery. Throughout history, people have searched for the secret to wealth. In truth, there is no single formula. Financial success comes from a blend of a positive and practical mindset, strong financial or business knowledge, refined skills, consistent effort, mental clarity, objectivity, creativity, strategic thinking, adaptability, and effective marketing. Even those with high incomes often feel financial pressure. The reason is simple: income alone does not guarantee financial security. For instance, an executive earning $500,000 annually may carry a $25,000 monthly mortgage—totaling $300,000 a year—along with taxes, utilities, insurance, car payments, groceries, tuition, and lifestyle expenses. As spending rises with expectations, the feeling of “not enough” persists. Behavior plays a critical role in financial outcomes. Impulsive spending, comparison with others, and the pressure to keep up can lead to poor decisions and mounting debt. Without addressing these habits and mindsets, achieving lasting financial stability becomes difficult. Our beliefs about money also shape our reality. Misinterpretations of ideas, even religious ones, can hold us back. The phrase “money is the root of all evil” is often misquoted. The accurate verse by Timothy states: "For the love of money is the root of all kinds of evil". This highlights that it's not money itself, but the love of money, or greed, which is the source of many problems. Limiting beliefs such as “I am not lucky enough” along with self-doubt and fear of failure, can prevent us from taking opportunities, planning effectively, and moving forward with confidence.

Understanding how money works

Understanding basic financial principles—such as income, expenses, saving, and investing—is essential for making sound decisions and building wealth. While this may seem straightforward, many people either mismanage their money or lack the skills to manage it effectively. Research shows that many people lack control over their daily income and spending. The first step toward gaining control is simple but powerful: track every transaction. Record your income and expenses daily using an app or spreadsheet. By doing this consistently, you gain a clear picture of where your money comes from and where it goes.

Taking Control

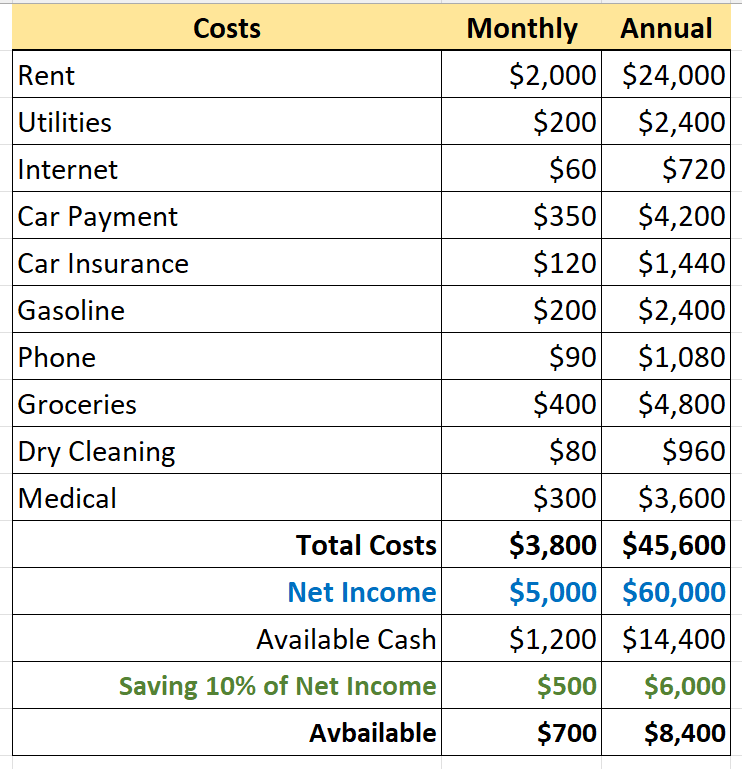

The most important step is gaining control over your expenses. Expenses generally fall into two categories. Fixed expenses stay relatively the same each month—these include rent or mortgage payments, car payments, insurance, internet service, and student loans. Variable expenses, on the other hand, fluctuate regularly and include costs like gas, groceries, utilities, medical bills, travel, clothing, entertainment, and dining out. By reviewing your expenses carefully, you can identify areas where you can cut back and reduce overall spending. Start with your fixed expenses and look for opportunities to lower them. For instance, you might reduce your monthly car insurance premium by increasing your deductible. Next, examine your variable expenses. These often include unnecessary purchases that gradually drain your finances. It’s important to distinguish between what you want and what you truly need. Many variable expenses are tied to habits—change the habit, and the cost decreases. For example, cutting back on how often you eat out can make a noticeable difference. Before making a purchase, ask yourself: Do I really need this now, or can I find it for less elsewhere? Am I paying with money I have, or am I borrowing through a credit card? The foundation of financial stability is simple: spend less than you earn and save what remains. A good guideline is to save 10% of your net income, which is what you take home after taxes and expenses. It’s a good idea to automate your savings by transferring a set amount from each paycheck directly into a savings account. In addition, aim to set aside 15% of your gross income, your earnings before taxes—into a retirement account. Building an emergency fund is also essential. If you live in a modern city, consider keeping around $2,000 in cash for immediate, short-term emergencies. Beyond that, aim to save at least six months’ worth of living expenses in a separate savings account. This fund can act as a financial safety net in situations like job loss or unexpected medical costs. While these goals may seem challenging, they are achievable and many disciplined and financially successful people follow these practices every day.

Handling Debts

All the emphasis on saving doesn’t matter much if we’re carrying debt. Debt refers to money we’ve borrowed—whether from loans, credit cards, car financing, or a mortgage. Living with debt can bring stress, anxiety, sleepless nights, and a constant sense of pressure and regret. As Benjamin Franklin put it, “When you are in debt, you give to another the power over your liberty.” The first step toward becoming debt-free is managing your mindset. Without the right perspective, it’s difficult to make progress. It’s important not to take debt personally or let it become overwhelming. Avoid denial and emotional reactions—instead, treat debt as a practical problem to solve. Start by listing all your debts so you have a clear picture. Then focus on paying off the smallest balances first to reduce clutter and build momentum. After that, prioritize debts with the highest interest rates to minimize long-term costs. Finally, turn your attention to larger balances as you continue working toward financial freedom.

Investing for Growth

Once we’ve built an emergency fund, paid off smaller debts, and established savings and retirement accounts, we can allocate part of our income toward investments aimed at growth. However, it’s important to do this using a disciplined and proven approach. We should avoid fraud and scams, and steer clear of overly risky ventures or deals that sound too good to be true. Any investment should prioritize safety and also be reasonably liquid, meaning it can be converted to cash within a sensible timeframe when needed.

Starting a Business

There are two primary ways to earn income: working for someone else or starting your own business. A traditional job can develop into a stable and fulfilling career when it is approached with intention and planning. It is important to be cautious about side hustles, gambling, or other high-risk ventures, as they often lead to financial loss and instability rather than long-term success or satisfaction. This raises an important question: should you follow your passion and pursue employment or entrepreneurship? Before starting a business, the first consideration is whether your passion aligns with real market demand. In other words, are people willing to pay for what you offer? It is also important to recognize that roughly 90% of new businesses fail, meaning that 9 out of 10 do not survive. Because of this, launching a business requires careful evaluation. You should determine whether your idea solves a real problem and whether there is genuine demand for it. It is not enough for an idea to simply be interesting or personally appealing to you, it must be something customers truly need and are willing to buy. You should also clearly define your target audience. Consider factors such as age, gender, income level, interests, and location. Another key factor is pricing. Low-cost products typically require high sales volume to be profitable, such as screws or nails. In contrast, high-priced items like luxury jewelry may sell in lower quantities but generate higher profit per sale. It is also important to research whether similar products or services already exist and evaluate their strengths and weaknesses. Finally, you should honestly assess your readiness. Are you prepared for long hours, stress, and uncertain income? Do you have access to the necessary resources such as time, money, and people? Can you handle financial risk and potentially go without steady income for a year or more? And do you have the knowledge and skills required to successfully deliver your product or service at a professional level?

Jobs and Career

Compared to business ownership, jobs typically provide more immediate financial stability and predictability. They often come with benefits such as health insurance, retirement plans, and other employee perks, along with a consistent weekly income that can be relied upon. However, employment also has its downsides. When working a job, you are ultimately working for someone else, which means having less control over your time, responsibilities, and overall direction. In addition, financial growth is often limited unless you intentionally focus on advancing your career. To achieve long-term growth, it is important to prioritize career development by building skills within a specific field or industry. Career planning can be approached through reverse planning: instead of starting from where you are and guessing the path forward, identify individuals who have already achieved the goals you aspire to. Then study their educational background, certifications, and professional journeys. From there, work backward to map out the steps you need to take starting today. It is also essential to consider how artificial intelligence and robotics may influence the future of your chosen career path.

Financial Stages of Life

When planning for long-term wealth, it is important to recognize that different stages of life require different financial strategies. Life’s financial journey typically unfolds in five distinct phases, and each one requires thoughtful planning tailored to its unique needs.

Early Adult

In early adulthood, the main focus should be on education and building a strong foundation for a future career rather than simply finding a job. One of the best first steps is to secure a reputable internship in a stable industry with a well-known company. Even if the internship is unpaid, it provides valuable experience and helps begin building a strong résumé and professional network. Minimizing or managing student debt can make a major difference in your financial future. For example, some universities offer free tuition if you work for the school. You must also open your first savings account and get into the habit of tracking your income and expenses every day. This builds strong money-management skills early on. You should begin building your credit history by getting a credit card with a low interest rate. Use it responsibly and pay off the full balance each month. Avoid charging more than you can afford to repay when the bill is due.

Early Career

In the early career phase, you should begin by building an emergency fund covering up to 6 months of your expenses. Plan to pay down debts including student loans and credit cards. Start a 401K retirement savings and IRA account. Read and learn about effective investing.

Professional Phase

In this phase, you should consider pursuing advanced education or specialized certifications to become experts in your field and differentiate yourself in the job market. At the same time, you should actively grow your professional network and personal brand. In this stage, financial discipline becomes increasingly important, with the goal of remaining debt-free whenever possible. You should plan for the future by investing in life insurance, retirement accounts, and college savings for children. A key long-term objective should be paying off home mortgage as quickly as possible in order to achieve full ownership and financial stability.

Pre-Retirement

In this phase the objective is to pay off all debts. Plan long term healthcare costs and coverage. Maximize retirement contributions. Shifting your investment toward lower risk and protecting what you’ve built includes completing essential estate planning and your will.

Retirement

The retirement phase is about slowing down and drawing income from savings, investments and Social Security as well as managing healthcare and long-term care costs.

Becoming Wealthy

Building wealth starts with establishing a strong financial foundation, as emphasized in this page. If someone cannot responsibly manage $2,000, they are unlikely to handle $20 million effectively. In fact, about 70% of lottery winners end up facing financial difficulties or even bankruptcy within a few years, largely due to excessive spending on luxury items such as homes, cars, vacations, and other non-essential purchases. Historically, wealth has been created through several key paths, including:

Inheritance

Building and scaling successful businesses

Owning equity in companies that grow significantly in value

Angel investing or venture capital, which involves funding early-stage startups with high growth potential

Private equity, where investors acquire, improve, and later sell businesses

Large-scale real estate development and investing in rapidly growing markets

Building a personal brand, audience, or expertise that evolves into a media-driven enterprise

Ultimately, developing wealth requires cultivating a mindset focused on growth and abundance, while actively learning financial principles, thinking creatively, and applying effective strategies to build long-term financial success.

WHAT IS WEALTH

PREPARATION

To get started, step away from your office or home and find a place where stress is minimal.

Take a pen and paper and be prepared to write down your ideas.

Start by listening to the audio session, then watch the short video(s).

Notice: The information on this page is intended for general informational purposes only and is not a substitute for professional accounting services or personalized financial advice.

GUIDED SESSION

Use headphones for optimal sound

Admiral McRaven

Founder of Apple Steve Jobs on Thinking about Money

Founder of Apple Steve Jobs on Simplifying

Income-Expenditure Relations, Elizabeth W. Gilboy. The Review of Economics and Statistics. Vol. 22, No. 3. Aug. 1940 p. 115-121. The MIT Press.

The Distribution of Income and Expenditure within the Household. Duncan Thomas. GENES. Jan. - Mar. 1993, pp. 109-135.

Evaluating Business Performance of Wealth Management Banks. Cheng-Ru Wu a, et al. European Journal of Operational Research. V. 207, Issue 2, 1 Dec 2010, P. 971-979.

On the Origin of Money. Karl Menger. Studies in the Static Foundations of Monetary Theory. 1989, P. 67-82.

The Rise of Digital Money. Tobias Adrian, et al. Annual Review of Financial Economics. V. 13, 2021.

The Transactions Role of Money. Joseph M. Ostroy, et al. Handbook of Monetary Economics. V. 1, 1990, P. 3-62. University of California Los Angeles.

Why Money? Armen A. Alchian. Journal of Money, Credit and Banking. Vol. 9, No. 1, Part 2. Feb. 1977, pp. 133-140.Ohio State University Press.